Key Takeaways

- GAP insurance protects you from owing more on your car loan than your vehicle’s market value if it’s totaled or stolen.

- Particularly useful for those with small down payments, long loan terms, or vehicles that experience rapid depreciation.

- Knowing precisely what GAP insurance covers and doesn’t cover is crucial for informed financial planning.

Understanding Vehicle Depreciation

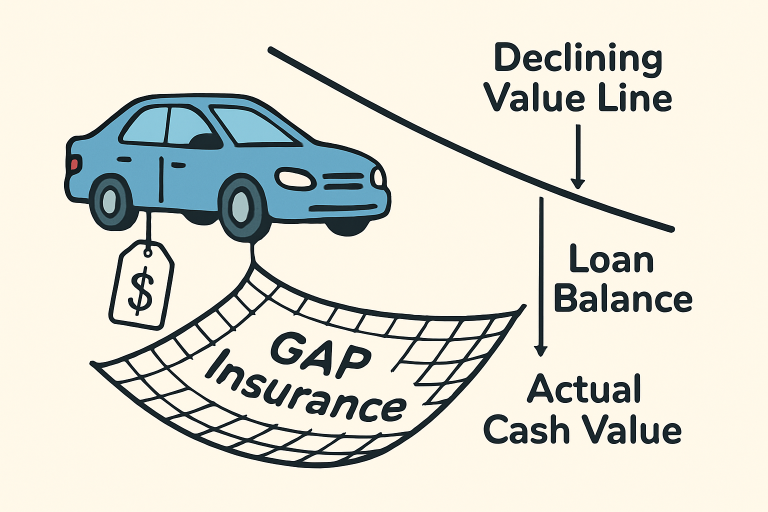

Driving a new car off the lot may be thrilling, but it comes with a hidden cost—depreciation. Most vehicles lose approximately 30% of their value within the first year and around 50% within three years. With standard auto insurance, you’ll often only receive your car’s depreciated, actual cash value if it’s declared a total loss. This sum is often much less than the amount still owed on an auto loan.

This is where the true value of GAP insurance becomes clear. If you’re in an accident or your car is stolen, GAP insurance fills the financial gap between your car’s reduced payout and your remaining loan balance. To clearly understand the coverage, it’s helpful to review what GAP insurance covers in typical policies.

Many Canadians underestimate how quickly their cars depreciate, especially with longer loans and minimal down payments. If you finance over 60 months or put less than 20% down, you risk paying out of pocket for a total loss. Leasing also increases this risk, as GAP insurance is often required. Knowing your car’s depreciation and how your loan compares helps protect your finances. For example, owing $25,000 on a car worth $20,000 after an accident leaves you responsible for the $5,000 difference. GAP insurance fills this gap, shielding you from debt and financial loss resulting from accidents or theft.

Who Should Consider GAP Insurance?

GAP insurance is beneficial for certain car owners under specific conditions. It is particularly valuable for individuals who have made a down payment of less than 20%, as they will owe more than the car’s value for an extended period. Those with loans longer than 60 months face an increased risk of negative equity due to the rapid depreciation of their vehicles. Owners of cars that tend to lose value quickly, such as luxury sedans and electric vehicles, also gain from this insurance. Additionally, borrowers who have rolled over negative equity from a prior loan introduce further risk to their new loan, making GAP insurance a valuable option. Many lenders and almost all leasing companies mandate GAP coverage for the financial protection it offers when owners have little or no equity stake in their vehicle at the beginning of the loan term.

Limitations of GAP Insurance

GAP insurance serves as a protective measure but has specific limitations. It is applicable only when a vehicle is declared a total loss due to severe collisions or theft, where recovery appears unlikely. Notably, GAP insurance does not cover overdue payments or late fees associated with loans, extended warranties, service contracts, previous vehicle loan balances, excess wear and tear penalties, or insurance deductibles. Understanding these exclusions can help avoid surprises during challenging times. Therefore, it is advisable to thoroughly review the policy details and inquire further before making a purchase.

Is GAP Insurance Worth the Cost?

GAP insurance is generally quite affordable, with costs varying depending on your provider and whether you buy it from a dealership, bank, or directly add it to your auto insurance policy. The real calculation is whether your potential financial exposure is worth the yearly or one-time premium. If your car loan exceeds your vehicle’s resale value by a significant amount, GAP insurance makes sense as a safety net.

On the other hand, if your loan balance is close to or less than the car’s value—perhaps due to a large down payment or if you’re nearing the end of your financing term—GAP insurance may not be necessary. Assess your risk carefully to make the most informed financial decision.

How to Obtain GAP Insurance

GAP insurance is available from several sources. You can purchase it at the dealership when buying or leasing a car, through your existing auto insurance provider as an add-on, or via the financial institution that arranged your loan. Shopping for quotes and reading the fine print is essential, as coverage amounts and costs can vary.

Compare options carefully. Ask your insurer and lender if you’re eligible for discounts, and ensure you understand the process for filing a claim should the worst happen. Being proactive can save you from unnecessary expenses and stress in the long run.

Conclusion

GAP insurance is a vital financial safeguard for anyone at risk of owing more than their car is worth—especially in the first few years of ownership. With vehicles losing value quickly and unpredictable incidents always possible, this type of coverage can offer invaluable peace of mind. Review your finances, understand your loan terms, and assess your risk to determine if GAP insurance aligns with your protection plan. Taking these steps ensures that your car loan is truly a pathway to financial freedom, not a source of stress.